Revocable vs. Irrevocable Trusts: Which is Right for You ?

When planning your estate in your 40s or 50s, choosing between a revocable trust and an irrevocable trust can feel overwhelming. Both serve important purposes, but for most people under 60, a revocable trust offers the flexibility and control needed during these dynamic decades of life. Understanding the key differences can help you make an informed decision that aligns with your current needs and future goals.

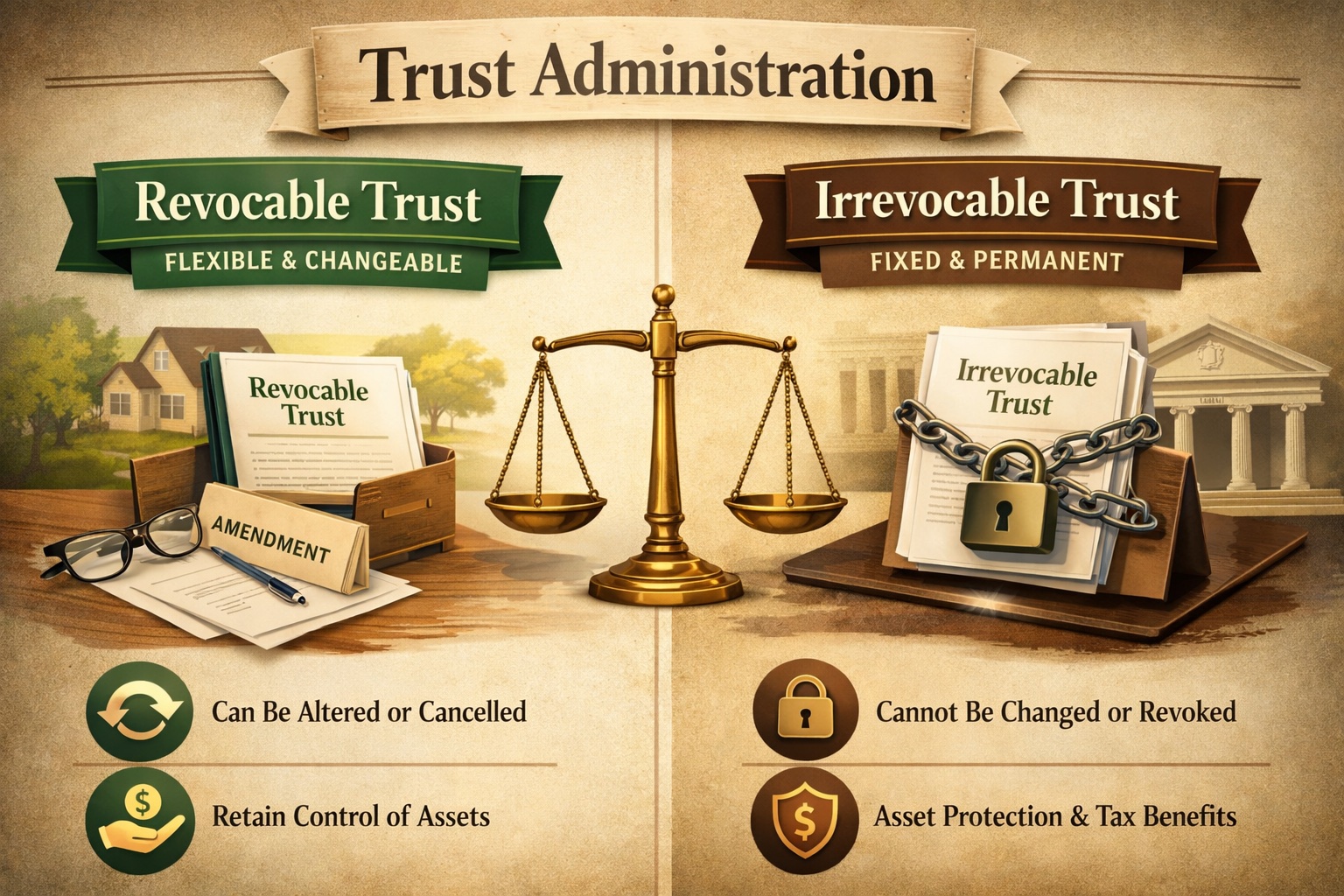

What's the Difference?

A revocable trust (also called a living trust) allows you to maintain complete control over your assets. You can modify, amend, or even dissolve the trust entirely at any time during your lifetime. You serve as the trustee, managing the assets as you always have, and can change beneficiaries or terms whenever your circumstances change.

An irrevocable trust, by contrast, transfers ownership of assets out of your control permanently. Once established, you generally cannot modify the terms, remove assets, or dissolve the trust without beneficiary consent or court approval. The assets no longer legally belong to you.

Why Revocable Trusts Work Better for Most People Under 60

Flexibility for Life's Changes

Your 40s and 50s are typically decades of significant change. You may experience career transitions, business ventures, divorce, remarriage, children going to college, or elderly parents needing care. A revocable trust adapts to these changes seamlessly. Need to refinance your home? No problem. Want to sell investment property? You maintain that authority. Circumstances change with a new grandchild or family member? You can easily update beneficiary designations.

With an irrevocable trust, you've locked yourself into decisions that may no longer make sense years down the road. The rigidity that provides asset protection can become a significant liability when life doesn't unfold as planned.

Maintaining Control of Your Assets

Most people under 60 are still actively building wealth, not just preserving it. You need access to your assets for opportunities and emergencies alike. A revocable trust lets you buy, sell, invest, and manage property exactly as you did before—because you still own it. You can respond to market opportunities, help children with unexpected expenses, or pivot your investment strategy without seeking anyone's permission.

Avoiding Probate Without Sacrificing Access

One of the primary benefits of any trust is avoiding the time, expense, and public nature of probate. A revocable trust accomplishes this goal while keeping you in the driver's seat. When you pass away, assets transfer to your beneficiaries privately and efficiently, often within weeks rather than months or years. You get this probate-avoidance benefit without giving up lifetime control.

Simpler Tax Reporting

Revocable trusts are "tax-neutral" during your lifetime. You report all trust income and deductions on your personal tax return using your Social Security number—no separate trust tax return required. This simplicity saves accounting fees and administrative headaches year after year.

Irrevocable trusts require separate tax filings and come with their own tax identification numbers. They may be subject to compressed trust tax rates, where income is taxed at the highest marginal rate much faster than for individuals.

Lower Setup and Maintenance Costs

Revocable trusts are generally less expensive to establish and maintain. Since you retain control and the assets remain in your estate for tax purposes, the legal work is more straightforward. Irrevocable trusts often require more complex drafting, ongoing legal and accounting support, and potentially court involvement for modifications.

When Might an Irrevocable Trust Make Sense?

Irrevocable trusts aren't inherently bad—they're just designed for specific situations that don't typically apply to people under 60:

Medicaid Planning: If you're facing long-term care needs and want to protect assets while qualifying for Medicaid, an irrevocable trust established well in advance (usually five years before applying) can help.

Significant Estate Tax Concerns: For 2024 and 2025, the federal estate tax exemption exceeds $13 million per individual. Unless your estate approaches this threshold, estate tax avoidance isn't a pressing concern for most people under 60.

Asset Protection Needs: If you face serious creditor threats or liability risks (certain high-risk professions, for example), an irrevocable trust can shield assets because you no longer legally own them.

Special Needs Planning: Irrevocable special needs trusts preserve government benefit eligibility for disabled beneficiaries without disqualifying them from essential programs.

For most professionals, business owners, and families under 60, these circumstances don't apply—or don't apply yet.

The Best of Both Worlds

Here's the key insight: you can start with a revocable trust now and convert assets to irrevocable trusts later if circumstances warrant. Many estate planning attorneys recommend establishing a revocable trust as your foundation while you're younger, then creating specific irrevocable trusts for targeted purposes as you approach retirement or face particular planning needs.

This staged approach gives you flexibility when you need it most, while keeping advanced planning strategies available for the future.

Making Your Decision

For most individuals and families under 60, a revocable trust provides the right balance of probate avoidance, privacy, incapacity planning, and flexibility. You maintain complete control over your assets while ensuring smooth transitions if something unexpected happens. As your circumstances evolve, your trust can evolve with you.

That said, every family's situation is unique. Complex business holdings, blended families, special needs children, or significant wealth may call for more sophisticated planning that includes irrevocable trusts alongside revocable ones.

Next Steps

Estate planning isn't one-size-fits-all, and the right trust strategy depends on your specific goals, assets, and family dynamics. At Gobena & Associates, we work with clients across North Carolina and Minnesota to develop comprehensive estate plans that provide protection today while remaining adaptable for tomorrow.

If you're under 60 and wondering whether a revocable trust makes sense for your situation, we invite you to schedule a consultation. We'll review your assets, discuss your goals, and create a plan that gives you peace of mind without sacrificing the flexibility you need during these important decades.

The information provided in this blog is for educational purposes only and does not constitute legal advice. Estate planning laws vary by state and individual circumstances. Please consult with a qualified estate planning attorney to discuss your specific situation.

Need Legal Assistance?

Contact Gobena & Associates for a consultation with our experienced attorneys.

Schedule Consultation